Amortization calculation is an essential tool in financial planning, allowing borrowers to understand the breakdown of their loan payments and the progression towards debt repayment.

Amortization calculation is an essential tool in financial planning, allowing borrowers to understand the breakdown of their loan payments and the progression towards debt repayment.

The process begins with the determination of the loan amount, interest rate, and loan term. Using this information, an amortization schedule is created, detailing each payment’s allocation towards interest and principal.

In the early stages of the loan, a significant portion of each payment goes towards covering the accrued interest, while a smaller portion goes towards reducing the principal balance. As the loan matures, the balance shifts, with a larger proportion of each payment allocated to principal repayment.

Amortization schedules provide borrowers with valuable insights into their loan repayment journey. They can see how much of each payment goes towards interest expenses and how much contributes to reducing the overall debt. This transparency enables borrowers to make informed financial decisions and plan for the future accordingly.

Furthermore, understanding the amortization process allows borrowers to assess the impact of different loan terms and interest rates on their repayment obligations. By adjusting these variables, borrowers can tailor their loan agreements to better suit their financial circumstances and goals.

Overall, amortization calculation plays a crucial role in empowering borrowers to manage their debt responsibly and work towards achieving financial stability.

Key TakeAway:

- Amortization refers to lowering the value of a debt or something intangible, such as a patent.

- Lenders, including banks, utilize amortization plans to indicate how a loan will be paid off by a specific date.

- When we amortize intangible assets, such as patents, we spread the cost over time to match the revenue they generate. It follows an accounting rule.

- Negative amortization occurs when loan payments are so little that the borrower owes more over time.

- Many accounting and spreadsheet tools can calculate amortization for you.

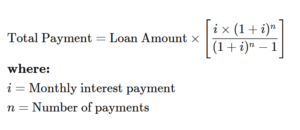

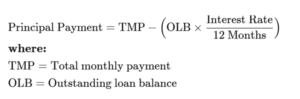

How to Calculate Loan Amortization?

Pros and Cons of Loan Amortization

| Advantages of Amortized Loans | Disadvantages of Amortized Loans |

|---|---|

| Level payments make long-term budgeting easier for individuals. | Relatively little principal is paid off in the early stages of the loan. |

| Each payment includes a principal component, reducing the outstanding balance over time. | Most of each payment goes toward interest initially. |

Why Is Amortization Important?

- Amortization helps businesses and investors plan their costs over time.

- Schedules show how much of a loan payment is interest and how much is principal.

- This clarity is useful for tasks like deducting interest payments on taxes and planning for future debt.

- Amortizing intangible assets can lower a business’s taxable income and help investors understand true earnings.

- Intangible assets, like trademarks, lose value over time, so amortization reflects their diminishing usefulness.

- Also shows how a company has benefited from and used up these assets.